Blog

What Are Mortgage Servicing Ratio and Total Debt Servicing Ratio (TDSR)?

Published 12 January 2026

Key Takeaways

- MSR (Mortgage Servicing Ratio) is capped at 30% of gross monthly income and applies only to HDB flats and Executive Condominiums (ECs).

- TDSR (Total Debt Servicing Ratio) is capped at 55% of gross monthly income and applies to all property loans (public and private).

- Stress Test Rate: Banks must use a minimum interest rate of 4% (or the prevailing rate, whichever is higher) when calculating your loan eligibility.

- Variable Income: Only 70% of variable income (e.g., commissions, bonuses) is counted towards these ratios.

In the process of finding the best home loan package? We understand how some mortgage terms can be confusing, especially for first-timers. If you’re taking a bank loan for your property purchase, there are key terms to understand when navigating the financial planning process.

All You Need to Know About MSR and TDSR

- Mortgage Servicing Ratio

- What is Total Debt Servicing Ratio (TDSR)?

- How does TDSR affect your home loan?

- What is the difference between MSR and TDSR?

- When do MSR and TDSR apply?

- Owning a Home Doesn't Have to be Financially Challenging

- Frequently asked questions about MSR and TDSR

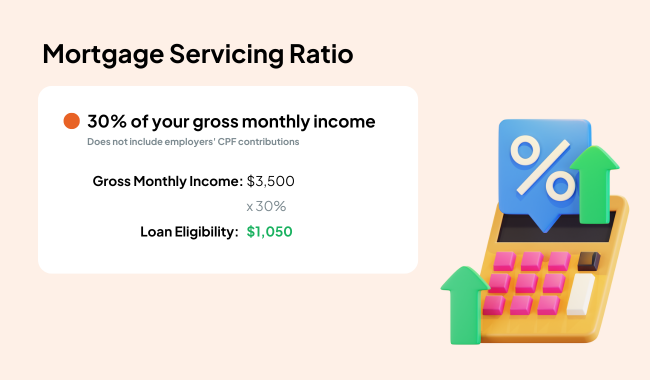

What is the Mortgage Servicing Ratio (MSR)?

Mortgage Servicing Ratio (MSR) is a home loan limit imposed by the Monetary Authority of Singapore (MAS). It applies to two types of properties: HDB flats (BTO and resale) and Executive Condominiums (bought directly from the developer). It caps the amount of the gross monthly income you can use to repay a loan at 30% (including employees’ CPF contribution). This ensures that you do not overleverage your mortgage payments alone.

How is MSR calculated?

For example, if you earn $3,500 per month, your loan eligibility is capped at $1,050 per month.

How is MSR calculated if you have a variable income?

If you have variable income (e.g., working freelance), you can only take 70% of your variable income for MSR calculations.

Example of MSR calculation

Alif is a full-time software engineer working in a multinational company, earning $4,000, and a freelance website developer, earning $3,000.

[Fixed Income + (70% x Variable Income)] x 30% = MSR

[$4,000 + (70% x $3,000)] x 30%

= ($4,000 + $2,100) x 30%

= $6,100 x 30%

= $1,830

Alif’s loan eligibility is capped at $1,830 per month.

What is Total Debt Servicing Ratio (TDSR)?

Total Debt Servicing Ratio (TDSR) is also a home loan limit implemented by MAS. It applies to both public and private properties. It was introduced in Singapore in 2013 by the Monetary Authority of Singapore (MAS) to:

- Promote responsible borrowing: The TDSR framework ensures that borrowers do not take on more debt than they can handle, preventing them from overextending themselves financially.

- Safeguard financial stability: By limiting the amount of debt individuals can take on, the TDSR helps to maintain the stability of the financial system and reduce the risk of a debt crisis.

- Curb property speculation: The TDSR was implemented in response to rising property prices, aiming to cool the property market by making it more difficult for individuals to borrow excessively for property purchases.

The TDSR framework has been adjusted over time, with the most recent change in December 2021 tightening the limit from 60% to 55% of gross monthly income. This means that borrowers’ total monthly debt repayments, including their mortgage, cannot exceed 55% of their gross monthly income.

What are the latest changes to TDSR?

While the TDSR threshold itself remains at 55% of gross monthly income, there have been recent changes affecting how it’s calculated and applied:

- Higher Medium-Term Interest Rate Floor: From September 30, 2022, MAS increased the medium-term interest rate floor used in TDSR (and MSR) calculations. This means banks must stress-test affordability at a higher interest rate, typically 4% per annum or the prevailing market rate, whichever is higher. This affects the maximum loan amount borrowers can qualify for.

- Lowered Loan-to-Value (LTV) Limit for HDB Loans: As of August 20, 2024, the LTV limit for HDB-granted housing loans was reduced from 80% to 75%. This means borrowers need a larger down payment for HDB flats.

- 15-Month Wait for Private Property Owners Buying Resale HDB Flats: Introduced as a cooling measure, private property owners below 55 years old now need to wait 15 months after selling their private property before they can buy a non-subsidized HDB resale flat. This indirectly affects TDSR as it impacts the pool of potential buyers and their financial situation when applying for loans.

These changes, while not directly altering the TDSR percentage itself, have made it tougher to qualify for the maximum loan amount due to the higher interest rate stress test and lower LTV limit. Additionally, the 15-month wait for some buyers can impact their financial planning and eligibility for loans.

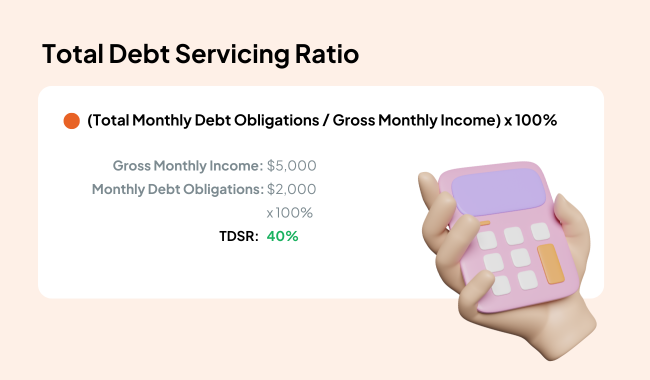

How is TSDR calculated?

In Singapore, TDSR is calculated using the following formula:

TDSR = (Total Monthly Debt Obligations / Gross Monthly Income) x 100%

Where:

- Total Monthly Debt Obligations: This includes all your monthly debt repayments, such as:

- Housing loans (including the one you’re applying for)

- Car loans

- Personal loans

- Student loans

- Renovation loans

- Credit card loans (minimum 3% of outstanding balance)

- Any other debt obligations

- Gross Monthly Income: This is your total monthly income before any deductions, including:

- Salary

- Bonuses

- Commissions

- Allowances

- Rental income (only 70% is considered)

- Other forms of income

Example of TDSR calculation

If your gross monthly income is $5,000 and your total monthly debt obligations are $2,000, your TDSR would be:

TDSR = ($2,000 / $5,000) x 100% = 40%

Since this is below the 55% threshold, you would be within the TDSR limit.

Example of TDSR calculation for those with variable income

How is TDSR calculated if you have a variable income? Those who have a variable income, such as self-employed freelancers, can only use 70% of their total income for TDSR calculations.

Michelle, a freelancer, earns $7,000 a month with an existing car loan of $1,000.

[(70% of variable income) x 55%] – outstanding loans = TDSR

= [(70% x $7,000) x 55% – $1,000)]

= ($4,900 x 55%) – $1,000

= $2,695 – $1,000

= $1,695

Michelle’s maximum home loan is capped at $1,695 per month.

How much can you afford for your next home? Get an automatic calculation today!

How does TDSR affect your home loan?

The TDSR limits the maximum amount you can borrow for your home loan. Since your total monthly debt repayments, including your prospective home loan, cannot exceed 55% of your gross monthly income, your existing debts directly reduce the loan amount you can qualify for.

Some other factors to consider

1. Longer loan tenure means lower monthly payments but higher total interest

If your desired loan amount results in a TDSR exceeding 55%, you might have to opt for a longer loan tenure to reduce the monthly instalments and bring the TDSR within the limit. However, this would lead to higher overall interest payments over the loan duration.

2. The TDSR is not your actual loan interest rate

The interest rate used for calculating the TDSR is not your actual loan interest rate but a higher stress-test rate (currently the higher of 4% or the prevailing market rate, after September 2022). This means the TDSR calculation assumes a higher monthly repayment for your home loan, further reducing the loan amount you can borrow compared to calculations using the actual interest rate.

What is the difference between MSR and TDSR?

MSR limits the amount of money you can borrow based on your income, without considering other loans you might have. TDSR takes into account ALL of your loan repayments, including outstanding non-mortgage loans.

If you’re buying an HDB or EC with a bank loan, you need to pass both criteria – MSR calculations followed by TDSR calculations.

Factors

MSR

TDSR

Definition

Proportion of gross monthly income used to repay all property loans

Proportion of gross monthly income used to repay all monthly debt obligations

Applicable Property

To ensure borrowers can afford their housing loan repayments, specifically for HDB flats and ECs

All property types

Threshold

30% of gross monthly income

55% of gross monthly income

Debt Obligations Included

Only property loans (including the one being applied for)

All debt obligations (property loans, car loans, personal loans, credit card debt, etc.)

Purpose

To ensure borrowers can afford their housing loan repayments

To ensure borrowers can manage their overall debt obligations without overextending themselves financially

Calculation

(Monthly repayment for all property loans / Gross monthly income) x 100%

(Total monthly debt obligations / Gross monthly income) x 100%

Who it Applies to

Borrowers applying for HDB or EC loans

All borrowers applying for property loans

Additional Notes

MSR is assessed first for HDB and EC loans, followed by TDSR

TDSR is the main criterion for loan eligibility for private property loans

Example calculation of MSR and TDSR

Clarence earns a fixed $5,000 monthly salary with a car loan of $1,000 and a study loan of $800.

First Criteria: MSR

Fixed Income x 30% = MSR

$5,000 x 30%

= $1,500

Clarence’s loan eligibility is capped at $1,500 per month.

Second Criteria: TDSR

Fixed Income x 55% = TDSR

$5,000 x 55%

= $2,750

Clarence’s monthly repayment for all debts cannot exceed $2,750.

Clarence’s outstanding loans:

$1,500 (MSR) + $1,000 (car loan) + $800 (study load) = $3,300.

Clarence’s bank loan can’t be approved because he did not meet the second criterion – his outstanding loans exceed $2,750. For such cases, you can reduce your obligations to pass the criteria for TDSR, i.e., take a lower loan amount or pledge to borrow a higher loan amount.

When do MSR and TDSR apply?

Loan Type

TDSR Applies?

MSR Applies?

HDB Flat Loan (from bank)

Yes

Yes

EC Loan (from bank)

Yes

Yes

Private Property Loan

Yes

No

HDB Loan (direct from HDB)

No*

Yes

*Note: HDB loans have their own set of eligibility criteria and loan limits.

When TDSR applies

- All Property Loans: TDSR applies to all property loans, regardless of the property type (HDB flat, Executive Condominium, or private property).

- New Loan Applications and Refinancing: TDSR applies to both new loan applications and refinancing of existing property loans.

When MSR applies

- HDB Flat and EC Loans: MSR applies specifically to loans taken for the purchase of HDB flats and ECs (where the minimum occupation period has not expired).

- New Loan Applications and Refinancing: MSR applies to both new loan applications and refinancing of existing HDB flat and EC loans.

When TDSR and MSR apply

HDB Flat and EC Loans from Financial Institutions: If you’re applying for a loan from a financial institution (bank or finance company) to purchase an HDB flat or EC, both MSR and TDSR thresholds will be considered. You must meet both criteria to be eligible for the loan.

Note: Loans directly from HDB are not subject to TDSR rules, but they have their own set of eligibility criteria and loan limits. However, MSR still applies to HDB loans.

Owning a Home Doesn’t Have to be Financially Challenging

Mastering MSR and TDSR calculations is a vital step in securing your next dream home, but it is equally important to understand the value of your current asset. Whether you plan to sell, refinance, or simply review your portfolio, taking the time to know your home’s worth ensures you are not leaving money on the table. With accurate market insights, you can navigate your property journey with confidence and clarity.

Frequently asked questions about MSR and TDSR

What is fixed income?

In MSR and TDSR calculations, the Monetary Authority of Singapore (MAS) defines fixed income as stable and regular earnings, like base salary, fixed allowances, and 100% of the employee’s CPF contribution. It excludes employer CPF contributions and variable incom,e like bonuses and commissions.

What is variable income?

According to the Monetary Authority of Singapore (MAS), variable income in MSR and TDSR calculations refers to earnings that are not regular or guaranteed. This includes bonuses, commissions, overtime pay, and any other income not considered stable and recurring. Financial institutions are required to apply a 30% haircut to variable income when calculating a borrower’s debt servicing ratios.

What is a joint application?

In a joint application for MSR and TDSR, the combined income (fixed and variable) and total debt obligations of all applicants are considered to determine the maximum loan amount and ensure affordability. The combined income increases the loan quantum while the combined debts affect the TDSR, ensuring responsible borrowing for all applicants collectively.

What are the TDSR exemptions?

There are no exemptions for TDSR in Singapore. However, the MAS allows refinancing for owner-occupied housing without being restricted by the TDSR threshold. Borrowers can also refinance investment property loans above the threshold under specific conditions and approval from the MAS.

Can I get a loan even if my TDSR is above the limit?

In exceptional cases, lenders may grant loans exceeding the TDSR limit, provided they have valid reasons and obtain MAS approval.

Does TDSR consider my spouse’s income and debts?

Yes, for joint applications, both incomes and debts are considered to determine the overall TDSR and MSR.

Are there any penalties for exceeding TDSR or MSR limits?

Exceeding the limits won’t incur penalties, but it will restrict your loan eligibility or amount.

Ready to sell your home? We’re ready to help.

Schedule a consultation with one of Singapore’s top agents.

Ready to sell your home? We’re ready to help.

Schedule a consultation with one of Singapore’s top agents.

Ready to sell your home? We’re ready to help.

Schedule a consultation with one of Singapore’s top agents.

Ready to sell your home? We’re ready to help.

Schedule a consultation with one of Singapore’s top agents.

Ready to sell your home? We’re ready to help.

Schedule a consultation with one of Singapore’s top agents.