Blog

4 Trends (+ 2 Myths) That Will Define Your Property Sale in 2026

Published 29 January 2026

Key Takeaways

- Supply Spike: Over 13,000 HDB flats will reach MOP in 2026, nearly double the supply of 2025.

- Interest Rates: Rates are stabilising at 3.0% – 3.5%, making strict budgeting essential.

- Right-Sizing Wave: Seniors will increase the supply of large flats while competing for 2- or 3-room units.

- Myth Buster: Waiting for a market crash is a losing strategy due to high holding costs.

- 4 Singapore Property Trends for 2026

- 2 Property Myths to Bust in 2026

- The Final Hurdle: The Simultaneous Trap

- Frequently Asked Questions (FAQ)

The familiar year-end rush of festive gatherings is here. As we wind down another busy year and look toward 2026, it is a natural time for reflection, reset, and planning. But if you are a homeowner thinking of selling, your biggest New Year’s resolution shouldn’t just be about health or travel — it should be about timing.

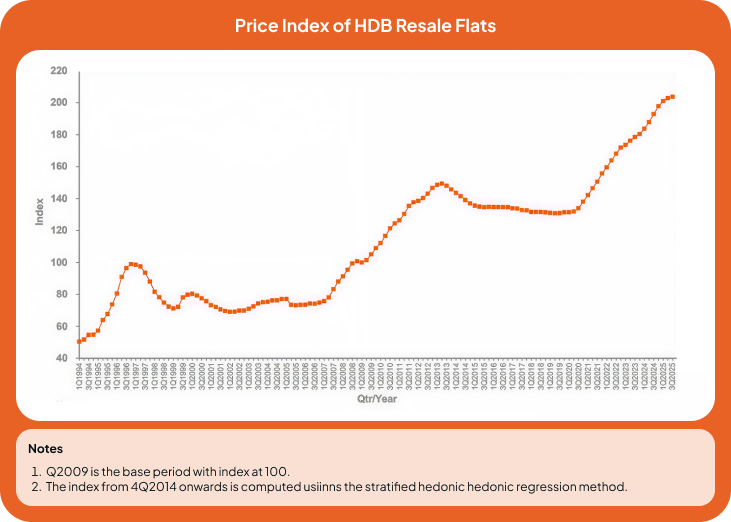

The last few years have been a whirlwind for the Singapore property market. We saw record-breaking transactions making headlines almost weekly, and Cash Over Valuation (COV) becoming a household phrase. However, as we enter 2026, the data points to a distinct shift. We are moving away from the post-pandemic frenzy into a period of stabilisation and smart strategy.

So, is 2026 a good time to sell? Yes, but the ‘easy sell’ era is over. You can no longer just post a listing and wait for a bidding war. Success in 2026 belongs to the sellers who understand the new playing field.

Here are the four trends that will define your sales in the year ahead, two popular myths you need to bust, and one critical operational hurdle you must plan for.

4 Singapore Property Trends for 2026

Trend 1: The Supply Spike

In 2025, the number of HDB flats reaching their Minimum Occupation Period (MOP) hit an 11-year low of roughly 7,000–8,000 units. This relatively low-supply environment helped keep prices buoyant.

What is changing in 2026? Market watchers project that the number of flats hitting MOP will nearly double to over 13,000 units in 2026. This increase in supply is largely due to construction delays from the pandemic years finally clearing up, releasing a wave of modern flats into the resale market.

Which estates will see a supply spike? If you live in Punggol, Tampines, or Toa Payoh, you need to pay close attention. These towns are expected to see the highest volume of fresh MOP flats for resale.

You are no longer the only shop open in your neighbourhood. With more options available, buyers can afford to be choosier. If you are selling a standard 4-room flat in Punggol, you will likely be competing against hundreds of similar units that have just MOP-ed.

Get an instant valuation for your home Access property insights and AI tools to maximise your property's potential and sell it fast Floor - Unit Property Type Home Type - Postal Code Get FREE valuation

Speed is critical. Listing early in the year — before the bulk of this new supply floods the property portals — could give you a competitive edge. To prepare, check how much your home is worth today through Ohmyhome’s Homer AI.

Trend 2: The Fixed Budget and Interest Rate Reality

While we have seen global interest rates dip slightly from terrifying peaks, the era of cheap money (remember those 1.5% mortgages?) is likely behind us for good.

Most analysts, including banks like OCBC and DBS, project the US Federal Reserve rates to settle near 3.5% in 2026. For Singapore homeowners, this means effective mortgage rates (SORA + bank spread) are likely to stabilise at 3.0%–3.5%.

How does interest affect your sale? It effectively caps the buyer’s budget. The Total Debt Servicing Ratio (TDSR) and Mortgage Servicing Ratio (MSR) frameworks mean that even if a buyer loves your renovation, the bank simply will not lend them more than their income allows.

The days of massive COV are dwindling. Buyers are price-sensitive, not because they are stingy, but because their loan eligibility is fixed. If you price your flat $50,000 above market value just to test the market, you risk your listing going stale.

Price accurately from day one. An overpriced listing doesn’t just sit; it gets stigmatised. Using data-backed valuation tools rather than guesswork is the only way to attract serious, qualified buyers who can actually secure the loan.

Trend 3: The Right-sizing Rush

Singapore is ageing, and by 2026, the ‘Silver Tsunami’ is expected to have a significant impact on the property market. Recent data indicate that nearly 1 in 3 HDB households is now led by a senior (65 or older).

Many of these owners are sitting on large, appreciated flats (5-room or Executive Maisonettes) in a mature estate and looking to right-size to smaller 2-room or 3-room flats or move to the new Community Care Apartments.

If you are selling a large flat in a mature estate like Ang Mo Kio or Bedok, you might see more competition from these right-sizers who are cashing out for retirement. Conversely, if you are selling a smaller unit, demand might remain robust as these seniors compete with young couples for 3-room flats.

Understand your buyer profile. If you are selling a large flat, market it to families that need space. If you are selling a compact unit, highlight its accessibility and elderly-friendly features (lift access, proximity to polyclinics) to attract the growing demographic of right-sizers.

Trend 4: The Digital Filter Effect

It is no longer enough just to post and pray. The buyer of 2026 is tech-first, likely a millennial or Gen Z who filters listings aggressively before booking a viewing.

Data shows that modern buyers spend less than 3 seconds deciding whether to click on a listing. If your property listing lacks a video tour, a clear floor plan, or immediate data transparency, it gets filtered out. They view 50 homes online but only visit three in person.

You need a strategy that puts your home in front of the right eyes. At Ohmyhome, our MATCH technology doesn’t just wait for buyers; it actively matches your property to a database of over 100,000 pre-qualified buyers based on their search criteria.

2 Property Myths to Bust in 2026

Myth 1: ‘I should wait for the crash’

You might have heard the whispers at the coffee shop: ‘Don’t buy or sell now, prices will crash soon.’

While price growth is moderating — analysts project a modest 1% to 5% growth for HDB resale prices in 2026 — a crash is highly unlikely. Singapore’s employment rate remains robust, and income growth is tracking steadily.

Furthermore, the government’s cooling measures act as a safety net. Just as they prevent prices from bubbling over, they also prevent the market from bottoming out. Waiting for a crash often means waiting while your next dream home gets more expensive (especially as private supply dips slightly in terms of new launches). Prices in Singapore are notoriously sticky — they rarely drop significantly unless there is a major global economic crisis.

Myth 2: ‘My renovation adds dollar-for-dollar value’

This is perhaps the most dangerous myth for 2026 sellers. ‘I spent $80,000 renovating the kitchen five years ago, so I should add $80,000 to my asking price.’

With construction costs expected to rise by 5% in 2026, according to Turner & Townsend, buyers do value a move-in-ready home. However, they value neutral renovations. They will not pay a premium for your specific taste in bold tiles or unique built-ins that they might have to hack away. In fact, extensive customisation can sometimes lower the value if the buyer calculates the cost of hacking it all down.

Focus on cosmetic staging rather than recouping renovation costs. A fresh coat of white paint and decluttering add more actual value to a sale than that expensive custom feature wall you installed in 2020. Of course, choosing the right renovation partner will set you up for success.

The Final Hurdle: The Simultaneous Trap

If you are a mover, 2026 presents a unique operational challenge: timeline. With the market moving at a moderate pace, you don’t want to sell your home too fast (and be left homeless) or buy your new home too early (and be stuck paying two mortgages or Additional Buyer’s Stamp Duty).

Managing the timeline of selling your HDB and buying a condo simultaneously requires precision. You need to align your Option to Purchase (OTP) dates, manage the HDB resale submission timeline, and sync up your loan disbursement.

This is where a Super Agent becomes essential. It’s not just about finding a buyer; it’s about project-managing your entire life transition so you never have to rent in between homes.

Ready to sell your home? We’re ready to help.

Schedule a consultation with one of Singapore’s top agents.

Ready to sell your home? We’re ready to help.

Schedule a consultation with one of Singapore’s top agents.

Ready to sell your home? We’re ready to help.

Schedule a consultation with one of Singapore’s top agents.

Ready to sell your home? We’re ready to help.

Schedule a consultation with one of Singapore’s top agents.

Ready to sell your home? We’re ready to help.

Schedule a consultation with one of Singapore’s top agents.

Make Your 2026 Move Count

2026 is shaping up to be a year of opportunity, but it favours the prepared. The market isn’t crashing, but it is becoming more competitive due to increased supply, with more discerning buyers constrained by fixed budgets.

Therefore, you can’t rely on luck. You need clear data, the right pricing strategy, and a team with Super Agents who know how to navigate the changing tides.

Ready to start your 2026 journey on a prosperous foot? Or do you have specific questions about your timeline? Drop us a message — we are here to help you make your next move the best one.

Frequently Asked Questions (FAQ)

Will HDB prices drop in 2026?

A massive price drop is unlikely, but price growth will likely slow down (stabilise) due to the increased supply of 13,000 MOP units entering the market.

Is 2026 a good time to sell my HDB?

It depends on your location. If you live in an area with many new MOP flats (like Punggol), you will face high competition. Selling before the full wave hits might be strategic.

What is the expected mortgage rate for Singapore in 2026?

Market projections suggest mortgage rates will hover between 3.0% and 3.5%.